net.sourceforge.jasa.agent

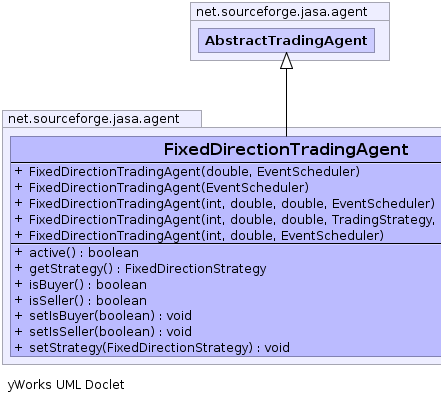

Class FixedDirectionTradingAgent

java.lang.Object

AbstractAgent

net.sourceforge.jasa.agent.AbstractTradingAgent

net.sourceforge.jasa.agent.FixedDirectionTradingAgent

AbstractAgent

net.sourceforge.jasa.agent.AbstractTradingAgent

net.sourceforge.jasa.agent.FixedDirectionTradingAgent

- All Implemented Interfaces:

- java.io.Serializable, java.lang.Cloneable, TradingAgent, MarketEventListener

- Direct Known Subclasses:

- TokenTradingAgent

public class FixedDirectionTradingAgent

- extends AbstractTradingAgent

-

-

| Fields inherited from class net.sourceforge.jasa.agent.AbstractTradingAgent |

account, currentOrder, group, initialFunds, initialStock, lastOrderFilled, lastPayoff, markets, stock, totalPayoff, utilityFunction, valuer |

|

Constructor Summary |

FixedDirectionTradingAgent(double privateValue,

EventScheduler scheduler)

|

FixedDirectionTradingAgent(EventScheduler scheduler)

|

FixedDirectionTradingAgent(int stock,

double funds,

double privateValue,

EventScheduler scheduler)

|

FixedDirectionTradingAgent(int stock,

double funds,

double privateValue,

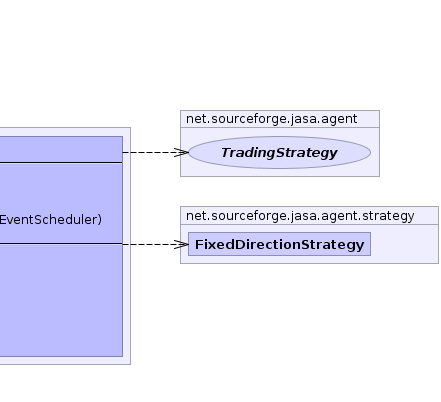

TradingStrategy strategy,

EventScheduler scheduler)

|

FixedDirectionTradingAgent(int stock,

double funds,

EventScheduler scheduler)

|

| Methods inherited from class net.sourceforge.jasa.agent.AbstractTradingAgent |

calculatePayoff, calculateProfit, clone, determineQuantity, equilibriumProfits, equilibriumProfitsEachDay, eventOccurred, getAccount, getCommodityHolding, getCurrentOrder, getFunds, getGroup, getLastPayoff, getMarket, getMarkets, getPayoff, getStock, getTotalPayoff, getTradingStrategy, getUtilityFunction, getValuation, getValuationPolicy, getVolume, giveFunds, initialise, isBuyer, isInteracted, isSeller, lastOrderFilled, onAgentArrival, onAgentArrival, onEndOfDay, onMarketClosed, onMarketOpen, orderFilled, pay, protoClone, register, reset, setGroup, setMarket, setMarkets, setPrivateValue, setUtilityFunction, setValuationPolicy, subscribeToEvents |

| Methods inherited from class java.lang.Object |

equals, finalize, getClass, hashCode, notify, notifyAll, toString, wait, wait, wait |

FixedDirectionTradingAgent

public FixedDirectionTradingAgent(EventScheduler scheduler)

FixedDirectionTradingAgent

public FixedDirectionTradingAgent(int stock,

double funds,

double privateValue,

EventScheduler scheduler)

FixedDirectionTradingAgent

public FixedDirectionTradingAgent(int stock,

double funds,

double privateValue,

TradingStrategy strategy,

EventScheduler scheduler)

FixedDirectionTradingAgent

public FixedDirectionTradingAgent(int stock,

double funds,

EventScheduler scheduler)

FixedDirectionTradingAgent

public FixedDirectionTradingAgent(double privateValue,

EventScheduler scheduler)

active

public boolean active()

- Description copied from class:

AbstractTradingAgent

- Determine whether or not this trader is active. Inactive traders do not

place shouts in the market, but do carry on learning through their

strategy.

- Specified by:

active in class AbstractTradingAgent

- Returns:

- true if the trader is active.

getStrategy

public FixedDirectionStrategy getStrategy()

setStrategy

public void setStrategy(FixedDirectionStrategy strategy)

setIsBuyer

public void setIsBuyer(boolean isBuyer)

isBuyer

public boolean isBuyer()

isSeller

public boolean isSeller()

setIsSeller

public void setIsSeller(boolean isSeller)