|

|

|

|

|

|

|

|||||||||

| PREV PACKAGE NEXT PACKAGE | FRAMES NO FRAMES | ||||||||

| Interface Summary | |

|---|---|

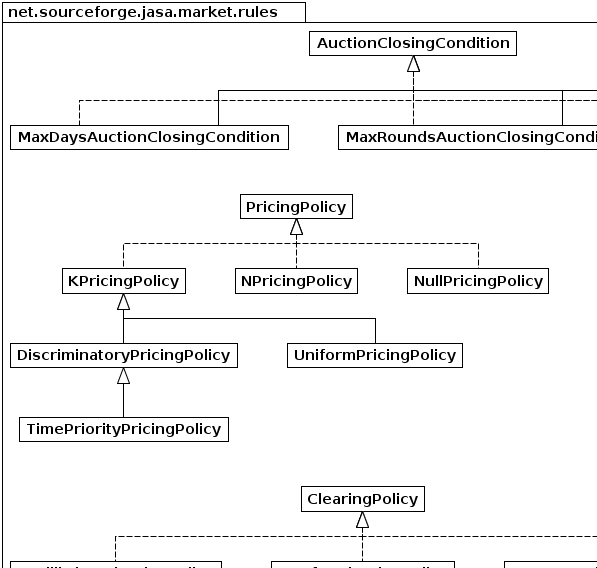

| AuctionClosingCondition | The interface for expressing the condition of closing an market. |

| ClearingPolicy | |

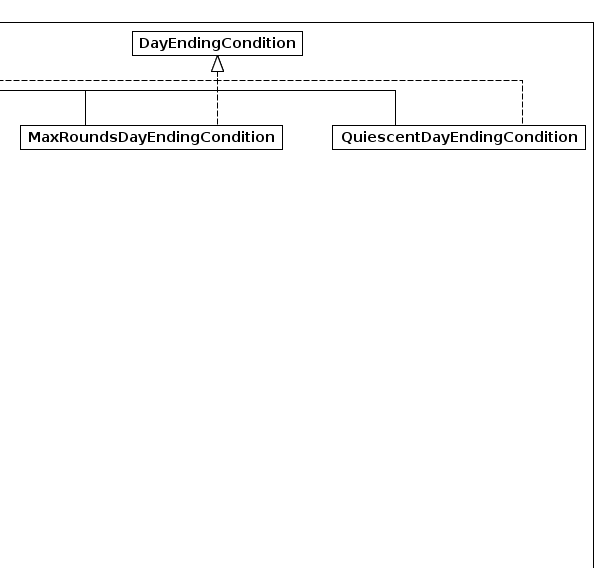

| DayEndingCondition | The interface for expressing the condition of ending an market day. |

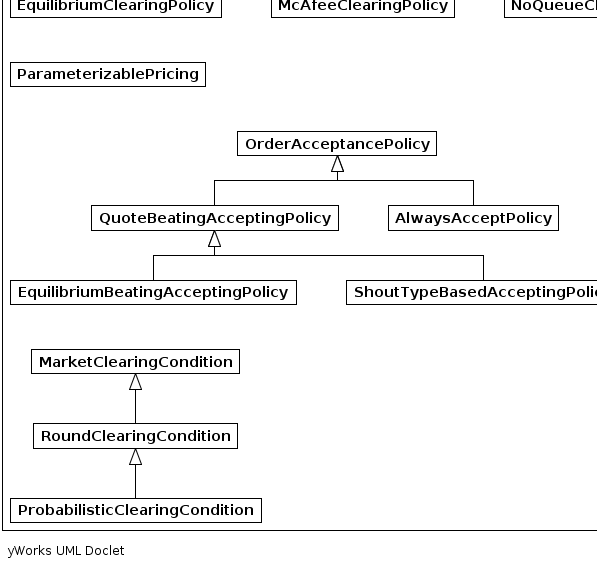

| ParameterizablePricing | Auctioneer classes implementing this interface indicate that they support parameterisable pricing rules, as per the k-double-market variants. |

| PricingPolicy | Classes implementing this interface define pricing policies for auctioneers. |

| Class Summary | |

|---|---|

| AlwaysAcceptPolicy | the losest accepting policy under which all shouts are allowed. |

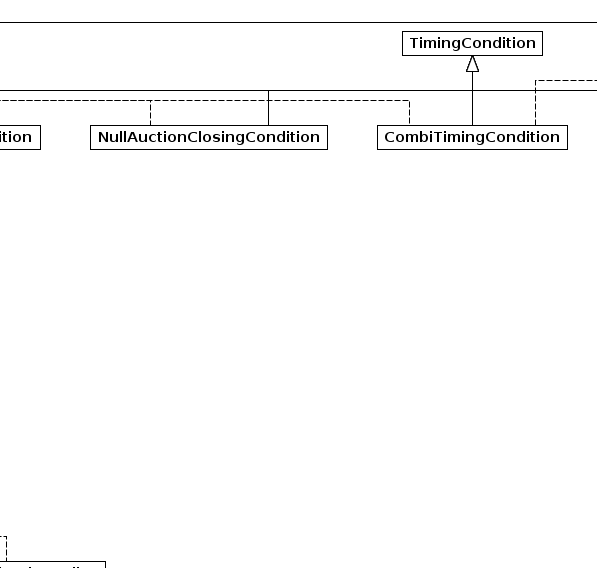

| CombiTimingCondition | The class for expressing the combination of timing conditions. |

| DiscriminatoryPricingPolicy | A pricing policy in which we set the transaction price in the interval between the matched prices as determined by the parameter k. |

| EquilibriumBeatingAcceptingPolicy | implements the shout-accepting rule under which a shout must be more competitive than an estimated equilibrium. |

| EquilibriumClearingPolicy | |

| KPricingPolicy | Abstract superclass for auctioneer pricing policies parameterised by k. |

| MarketClearingCondition | The interface for expressing the condition of clearing the current market. |

| MaxDaysAuctionClosingCondition | The interface for expressing the condition of closing an market. |

| MaxRoundsAuctionClosingCondition | The interface for expressing the condition of closing an market. |

| MaxRoundsDayEndingCondition | The interface for expressing the condition of closing an market. |

| McAfeeClearingPolicy | An implementation of the mechanism described in "A Dominant Strategy Double Auction" R. |

| NoQueueClearingPolicy | |

| NPricingPolicy | A discriminatory pricing policy that uses the average of the last n pair of bid and ask prices leading to transactions as the clearing price. |

| NullAuctionClosingCondition | |

| NullPricingPolicy | |

| OrderAcceptancePolicy | Classes implementing this interface define policies for accepting shouts. |

| ProbabilisticClearingCondition | The class for expressing whether the market should be cleared or not. |

| QuiescentDayEndingCondition | The interface for expressing the condition of closing an market. |

| QuoteBeatingAcceptingPolicy | implements the NYSE rule under which a shout must improve the market quote to be acceptable. |

| RoundClearingCondition | The interface for expressing the condition of clearing the current market. |

| ShoutTypeBasedAcceptingPolicy | implements the shout-accepting rule under which a shout must be more competitive than an estimated equilibrium. |

| TimePriorityPricingPolicy | Set the transaction price at the price of the order which arrived at the market first. |

| TimingCondition | The interface for expressing the condition of closing a certain time interval, such as an market, or a day, or whether it's time to do something, i.e. |

| UniformPricingPolicy | A pricing policy in which we set the transaction price in the interval between the ask quote and the bid quote as determined by the parameter k. |

|

|

|

|

|

|

|

|||||||||

| PREV PACKAGE NEXT PACKAGE | FRAMES NO FRAMES | ||||||||